Direct Market Access

Darwinex offers direct market access (DMA) to all its customers and guarantees that it will never trade against them. This means that Darwinex and its customers have no conflict of interest.

One of the obligations imposed by the FCA (UK), CNMV (UE) and FSA (Global) on brokers is to always offer its clients the best price available on the market. In order to do so, we are connected to the main liquidity providers around the world through different sources.

A trade's ''journey''

When a client sends an order from their trading platform, it starts a ''journey'' until it is finally accepted and executed by one of our liquidity providers.

How a trade is executed depends on whether the asset is traded over the counter (OTC) or on an exchange. Currencies and contracts for differences (CFDs) are -for the time being- traded over the counter.

How are orders executed at Darwinex?

Here is the ''journey'' that a currency and CFD trades undergo at Darwinex.

1. Sending the order from the trading platform

When a trader wishes to trade they must send the order from their trading platform, together with the volume required.

Depending on where the order is sent from, and the trader's Internet connection, this can be delayed by an average of between 100 and 200 milliseconds.

2. Arrival to the broker's central server

The order travels via Internet to our server.

In the case of Darwinex, the central server is located in Equinix LD4, London.

3. Requesting the best available price

Once the order has arrived to the server, our Prime Broker offers the best price available at that moment from all of the prices offered by the liquidity providers that act as a counterparty.

Darwinex offers liquidity from more than 20 different providers, amongst which the world's most important banks can be found, who have up to 200 milliseconds to accept the trade.

4. Acepting the trade and trade execution

Once the trade is accepted the relevant accouting entries are produced so the trade is recorded, meaning the trade is confirmed and executed.

During this process, the price at which the order is executed could have varied for two reasons:

- Latency. From the time that the order is sent until it is executed there is a time delay, or latency. During this time interval, the asset price may have moved, in your favour or against you.

- Market depth. If at the moment that the trade arrives to the market there is not enough volume at the best available price, the trade ''sweeps'' market depth at the different price levels available until the trade is completed for all of the requested volume. This implies that the final price obtained will be average of the best price available in the different liquidity sections.

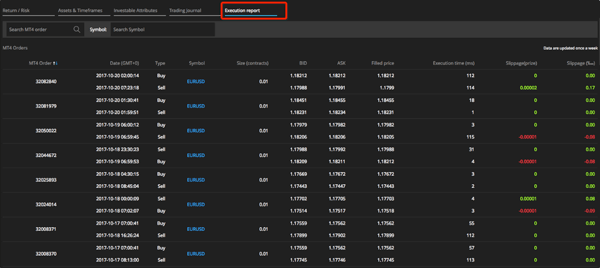

Execution quality at Darwinex

Darwinex traders may cross-check, for every filled order, the requested vs. the fill price and well as round-trip latency.

They can do this in the Execution report of their strategy.

Related articles

- Bid/Ask spread (covering best available price / Top of Book price)

- Will Darwinex become a market maker?

Related videos and podcasts

- On how exchanges and their central counterparty (CCP) work, what kind of order types there are and how they work.

- On how OTC trading works as opposed to on-exchange trading and what exactly an electronic communications network (ECN) is.

- On market participants of OTC markets and how they relate to each other.

- On marketing buzzwords in trading like DMA, ECN or STP.

- Podcast on liquidity aggregation at our brokerage. We explain where the price you see and where the price you get come from when trading the assets we offer.

- Webinar recording on how a pure A-Book broker prices spot FX for you. We explain the terminology (Liquidity Providers, Takers, Prime Brokers, etc.) and how OTC and on-Exchange markets differ. Last, but not least, we explain how flash crashes come about on the basis of an example affecting our brokerage.

- Webinar recording on slippage. Why it happens plus we introduce the tools to disclose slippage at our brokerage.